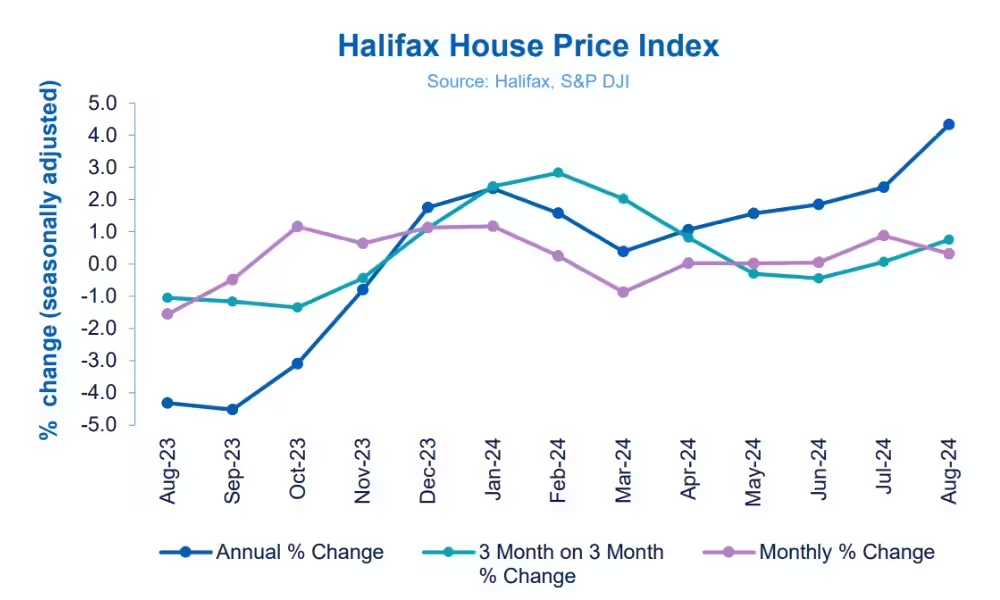

Halifax Cuts Mortgage Rates: New Opportunities for Low-Deposit Borrowers

In recent mortgage news, Halifax has confirmed improved rates for low-deposit mortgages, offering a glimmer of hope for first-time buyers and those with limited upfront capital. The lender, one of the UK’s largest, has introduced significant rate cuts across its mortgage products, particularly benefiting those with smaller deposits. This move comes amidst a backdrop of reduced competition in the mortgage market, as inflation and rising interest rates have made borrowing more expensive in recent months.

Key Changes in Mortgage Rates by Halifax

Halifax has reduced rates by up to 0.46 percentage points, specifically targeting borrowers with a loan-to-value (LTV) ratio of 90% or higher. Borrowers with larger deposits, such as 40%, also see reductions, with their five-year fixed rates decreasing to 4.53%. These deals typically come with a £999 fee, but for many borrowers, the reduced interest rates could make long-term mortgage payments more manageable.

These changes align Halifax with other major lenders like HSBC and First Direct, who are also adjusting rates in a more borrower-friendly direction. While average rates across the market have hovered above 5%, Halifax’s cuts signal that more affordable borrowing options are starting to re-emerge, which could be critical for revitalizing a sluggish housing market. Some experts believe this trend might continue as more banks compete to attract customers in a challenging economic climate(The Independent).

Impact on Low-Deposit Borrowers

One of the most notable aspects of these rate reductions is the improved accessibility for first-time buyers, who often struggle to amass large deposits. In an environment where property prices remain high and wage growth has lagged, Halifax’s improved rates for 90% and 95% LTV mortgages are designed to help people with smaller deposits enter the market.

Halifax’s move follows a wave of similar actions by other lenders in the market, reflecting a shift in the financial sector towards making mortgages more affordable. This is particularly important as inflation remains elevated, and the Bank of England’s base interest rate has been rising. Many potential buyers have been waiting for rates to drop before entering the market, and this recent reduction could encourage more people to take the plunge(Evening Standard).

Broader Market Trends

Halifax’s rate cuts come at a time when the property market has been under pressure due to increasing interest rates. Over the past year, the Bank of England raised interest rates 14 consecutive times in an effort to combat inflation, leading to higher mortgage costs. However, recent months have seen a stabilization in these rate hikes, offering some relief to potential homebuyers. While rates are still higher than they were during the pandemic lows, the latest cuts are a positive sign that mortgage rates could continue to decline.

Additionally, experts believe that while we may not see mortgage rates return to their previous lows, the current cuts are a step in the right direction, making mortgages more affordable for a broader range of people. This is crucial, as many buyers had been priced out of the market due to the rising costs of borrowing(The Independent).

Conclusion

Halifax’s recent rate reductions represent a significant shift in the mortgage landscape, particularly for first-time buyers and those with low deposits. With cuts reaching as much as 0.46 percentage points for certain fixed-rate deals, Halifax is positioning itself competitively against other lenders like HSBC and First Direct. While rates remain higher than in recent years, these reductions could provide much-needed relief for prospective homeowners and stimulate renewed activity in the housing market.

As more banks join the trend of rate cuts, it is possible that borrowing costs will continue to decrease, potentially leading to a resurgence in demand for housing. However, it remains important for borrowers to carefully assess their financial situation and consider the long-term affordability of their mortgage in an environment where rates may fluctuate.

Stay tuned for more updates…